SBTi Corporate Net-Zero Standard V2.0: Major Changes to Scope 1, 2, 3 Targets & Climate Transition Plans

/

The Science Based Targets initiative (SBTi) is currently updating its Corporate Net-Zero Standard (CNZS), with Version 2.0 (V2.0) expected to be finalized and published in 2026. This update represents a significant evolution over CNZS Version 1.3, introducing changes from the Draft for Second Public Consultation (Nov 2025), such as individual Scope 1, 2, and 3 (by Scope 3 category) target-setting approaches, third-party assurance requirements, and mandatory Climate Transition Plans.

The proposed changes from the Draft (Nov 2025) are extensive, but they can be understood through a few key structural shifts:

Two categories for entities to determine the applicability of requirements

Required Climate Transition Plan

Required third-party assurance

Three methods for Scope 1 target-setting

Updated Scope 2 target-setting

Three approaches for Scope 3 target-setting

Two-Tiered recognition model for addressing ongoing emissions

This article highlights key proposed updates from the second consultant draft of the Standard, along with the expected implementation timeline and validation process. SBTi has not yet released a specific publication date for the final V2.0 in 2026.

What is the Corporate Net-Zero Standard (CNZS)?

SBTi maintains a suite of Standards, including two cross-sector standards: the CNZS and the SBTi Financial Institutions Net-Zero (FINZ) Standard, as well as multiple sector-specific standards.

The CNZS serves as the foundation for all companies setting science-based targets, from which companies must determine whether additional SBTi Sector Standards apply to their operations.

All Companies are required to meet the full set of CNZS criteria, in addition to any applicable Sector Standard requirements.

The applicability of each Sector Standard, including associated metrics, methods, pathways, and whether requirements are optional or mandatory, is outlined in Table A.1, Annex A.

Companies that generate 5% or more of their revenue from financial activities must apply the FINZ Standard for their Scope 3, category 15 emissions.

Key Elements of the CNZS V2.0 Draft

The second consultation draft of CNZS V2.0 introduces a series of structural and technical updates that reshape how companies set, validate, and report net-zero targets. These updates can be understood through several key components.

Two Categories for Entities: Category A and Category B

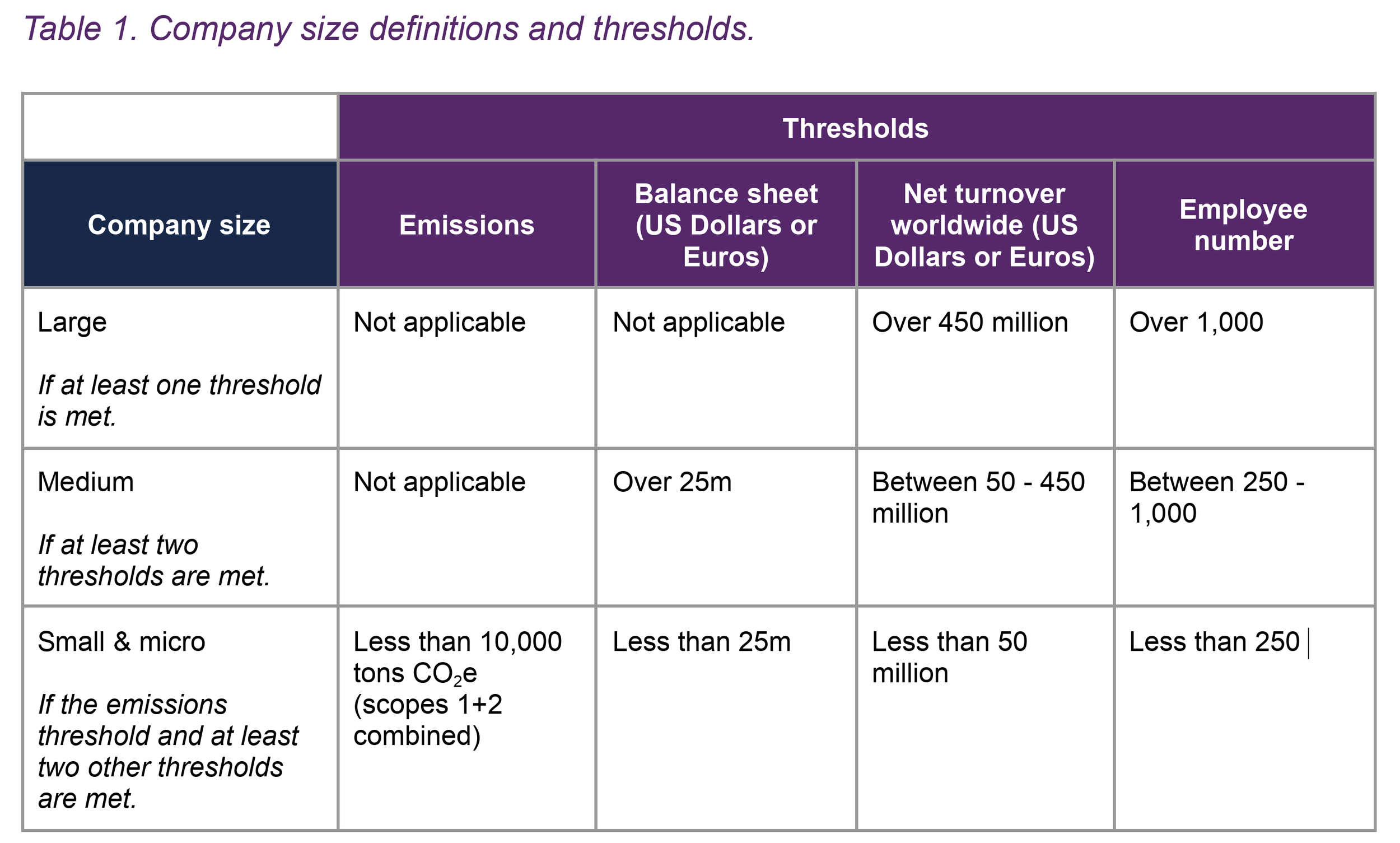

CNZS V2.0 includes two company classifications: Category A and Category B, which determine the applicability of specific criteria based on company size and geography.

| Category A Companies | Category B Companies |

|

|

Full, detailed definitions and thresholds for these categories are provided in Table 1 and Table 2 of section A.5 in CNZS V2.0.

Published Climate Transition Plan within 12 Months of Validation

Category A companies will be required to develop a Climate Transition Plan and publish it within 12 months of initial validation. Category B companies are encouraged, but not required, to do so.

The Climate Transition Plan must include:

Target details

A high-level roadmap of actions:

Near-term (0-5 years): concrete actions

Medium-term (5-15 years): indicative actions

Long-term (15+ years): consistency with net-zero

Assumptions and dependencies

Fossil fuel phase-out considerations

Costing

Approval

A five-year review cycle

Third-party Assurance on Calculated Values for Metrics Used in Target Setting

Third-party assurance will be required for Category A companies (optional for Category B).

Assurance must cover:

Scope 1, 2, and significant Scope 3 categories

Any relevant metrics used in their targets (see Table A1 and Table A.3 in Annex A)

Assurance must be performed by an independent third-party verification provider accredited by a recognized body and conducted in accordance with internationally recognized standards. (The SBTi provisionally considers the CDP list of accepted verification standards as recognized standards.)

The minimum level of assurance required was identified as a key area of consultation in the draft.

Three Methods for Scope 1 Target-Setting

CNZS V2.0 has three proposed methods for setting Scope 1 targets:

Emissions Metric Targets: Reducing emissions on a linear pathway to net-zero. Targets may be set on an absolute basis using the Linear Contraction method and/or on an intensity basis using the Sectoral Decarbonization Approach.

Alignment Targets: Increasing the share of low-carbon activities over time at a rate consistent with the reference pathways.

Asset Decarbonization Plan Targets: A roadmap-based approach to decarbonize assets, based on technological readiness and supported by a company-specific carbon budget to reflect sectoral realities.

Updated Scope 2 Target-Setting with Strengthened Integrity

All companies will be required to align with 100% low-carbon electricity by 2040 at the latest. Key elements include:

Low-carbon Electricity Targets:

Organizations must linearly increase the percentage of low-carbon electricity they procure or match (e.g., through Energy Attribute Certificates (EACs)) to reach 100% by 2040. “Low-carbon electricity” is defined as ≤ 0.024 kg CO₂ per kWh.

V2.0 will have stronger requirements for contractual instruments under the market-based method, including:

Geographic matching requirements, ensuring that purchased instruments are sourced from the same grid region as electricity consumption.

Establishing temporal matching as a “north star”, encouraging alignment between when electricity is consumed and when low-carbon generation occurs.

Three Approaches for Scope 3 Target-Setting

The draft refocuses Scope 3 target-setting on the highest-impact value chain emission sources, while allowing for exclusions on lower-impact or lower-influence value chain activities.

It introduces flexibility in how companies can implement Scope 3 targets, including approaches at the:

Emission source level

Counterparty level

Activity-pool level

Sector level

The V2.0 draft also introduces the limited use of high-quality environmental attribute certificates.

The three Scope 3 target-setting approaches include:

Emissions Intensity Targets: Targets based on reducing emissions intensity across relevant Scope 3 activities.

Activity Alignment Targets: Targets focused on aligning specific activities with low-carbon pathways.

Counterparty Alignment Targets: Targets based on cascading engagement through the supply chain to drive emissions reductions.

Two-Tiered Recognition Model for Ongoing Emissions

The V2.0 draft introduced an optional recognition program for companies to address ongoing emissions. Companies can earn recognition through two tiers – “Recognized” and “Leadership” – that have differing levels of responsibility:

Recognized: Companies must take responsibility for a minimum of 1% of ongoing scopes 1-3 emissions over the target timeframe.

Leadership: Companies must take responsibility by applying a carbon price to 100% of ongoing emissions.

Addressing ongoing emissions will remain optional until 2035, at which point it will become mandatory for all Category A companies to take responsibility, with the applicable threshold level to be determined.

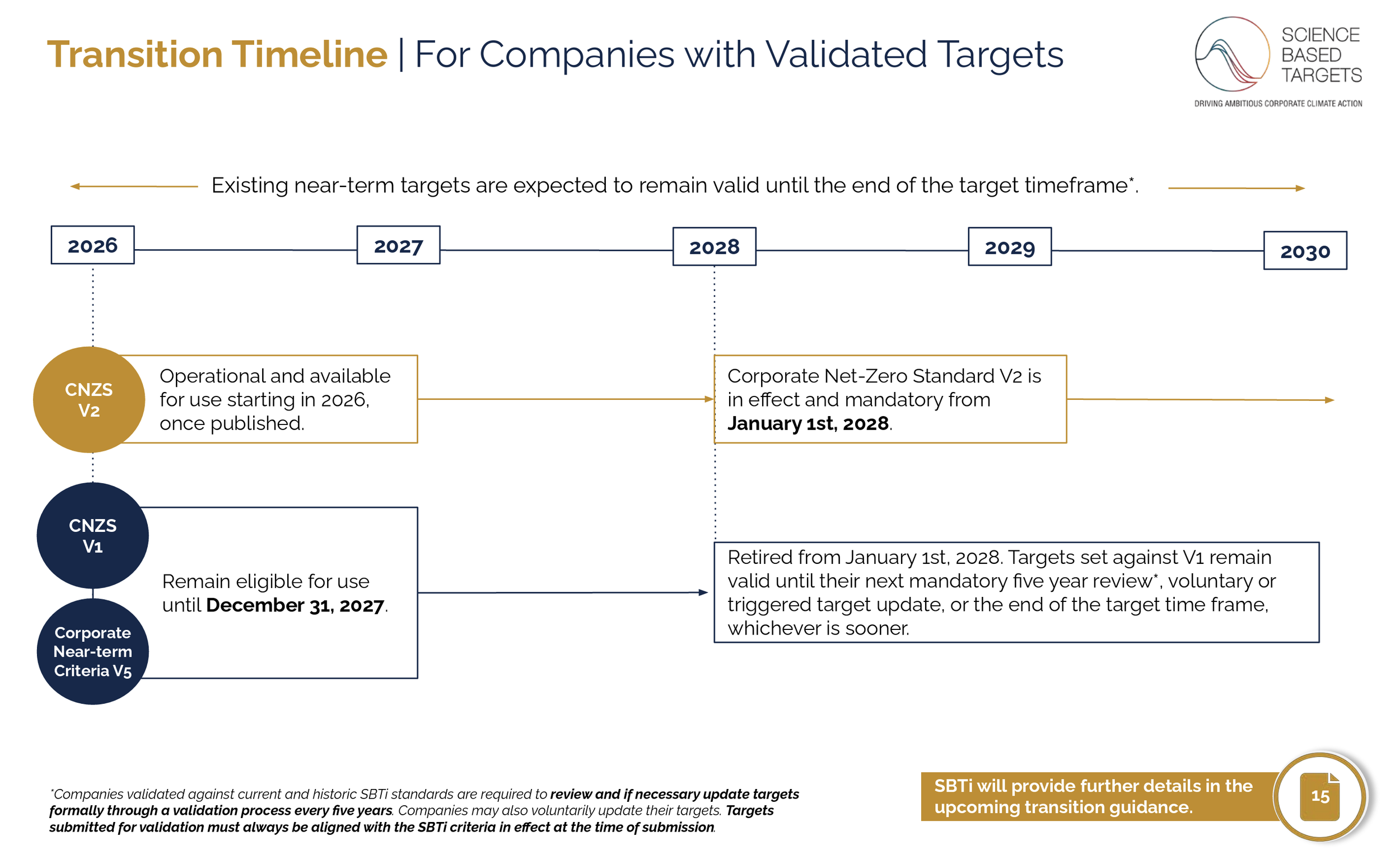

Timeline for CNZS V2.0 Adoption

While V2.0 is expected to be published in 2026, it will not become mandatory until January 1, 2028. SBTi has proposed a transition period between the current CNZS V1.3 and the upcoming V2.0 to allow companies time to adapt to the new requirements.

Companies may continue to set new targets under the current CNZS V1.3 and Near-Term Criteria (V5.3) until December 31, 2027. From January 1, 2028, all companies will be required to use V2.0.

Companies with Existing Commitments: Will be required to use the version of the Standard that is in effect at the time of target submission.

Companies with Existing Near-Term Targets: Will remain valid until the end of the defined target timeframe.

KERAMIDA helps companies set and achieve science-based emissions-reduction targets aligned with the SBTi, from establishing your emissions inventory baseline to submitting and validating your targets. Schedule a call with one of our SBTi experts to get started.

Author

Erica Skowron, MS, LEED GA

Senior Manager, GHG & Sustainability Data

KERAMIDA Inc.

Contact Erica at eskowron@keramida.com

Related Services

At KERAMIDA, we help companies set and achieve science-based emissions-reduction targets aligned with the Science-Based Target Initiative (SBTi). We guide organizations through every stage of the SBTi journey — from establishing your emissions inventory baseline to submitting and validating your targets.

KERAMIDA offers a wide variety of Greenhouse Gas (GHG) services to clients worldwide, including multi-facility industrial clients, industrial associations, law firms, and state organizations. Our experienced team of GHG experts provides carbon footprint evaluations, GHG inventories, GHG monitoring plans, and training.

Trusted for Verification and Assurance by Fortune 500 companies from a major U.S. stock market index and a global media & entertainment conglomerate to one of the largest U.S. steel producers and a world leader in marine recreation. KERAMIDA provides independent verification and assurance of GHG emissions for organizations across any industry in accordance with a variety of accepted standards, including ISO 14064-3 standards. KERAMIDA is a CDP Global Gold Verification Provider and an AA1000 Licensed Assurance Provider.

KERAMIDA develops GHG emissions inventories that are accurate, defensible, and ready for investor and regulatory scrutiny. We quantify Scope 1 (direct), Scope 2 (purchased energy), and Scope 3 (value chain) emissions using the best available organizational data and acceptable methodologies as defined by the GHG Protocol. Whether you have detailed primary data, utility bills, fuel usage records, procurement spend, or supplier-provided estimates, our team can work with what is available to create a complete and transparent accounting of your emissions inventory.